The New York Times once described him as someone who “chases deals, the way a dog chases cars”.

If you thought that was derogatory, you misunderstood. In fact, some would call it a rather benign description. His adversaries know for a fact that when he narrows down on a target, he goes for the kill. He is relentless and formidable.

Apparently, he bristles at being referred to as a ruthless corporate raider. But frankly, that is a courteous label when compared to the ultimate corporate predator, vulture capitalist, the Wall Street agitator, the Breakup Master, an icon of ‘80s greed and, most dramatic of all, “an evil Captain Kirk”. The most magnanimous probably being activist investor.

His favorite Italian restaurant in New York, Il Tinello, has a dish named after him: Pasta alla “Icahn.” (I checked out the menu, it’s true). And why would they do that? Well, those are some of the perks of being one of the richest men in the world.

You obviously would have guessed by now that I am talking about billionaire Carl Icahn. Currently worth around $19 billion.

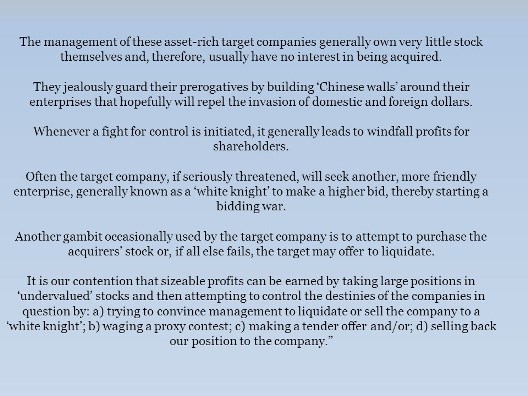

His strategy of identifying undervalued companies, acquiring a very significant stake in them, and employing various tactics to bridge the gap between book and market value, and come away with obscene amounts of money, is legendary.

Using Benjamin Graham’s investment philosophy as a foundation, Icahn pursues deeply undervalued positions offering asymmetric returns. For instance, he picked up U.S. casino operator Tropicana Entertainment in 2008 when it was in the throes of bankruptcy. He turned it around and in April this year cashed out with a sale of $1.85 billion to Eldorado Resorts.

What is unique to his style, is that he often looks for stakes in companies where he can control his destiny. If one looks at his track record, it reveals that he virtually mirrors the evolution of shareholder activism.

One of his biggest wins was cancer drug developer ImClone Systems. In 2006, Icahn won control after an intense proxy battle and rejected a $36-a-share takeover offer. He became the chairman and again rejected a takeover offer by Bristol-Myers at $62. In 2008, ImClone accepted a $70-a-share bid from Eli Lilly & Company. The New York Times stated that in a 2006 interview, Icahn claimed that he paid less than $20 a share for much of his initial investment. Got the idea?

In the 1932 The Modern Corporation and Private Property, Adolf Berle and Gardiner Means argued that modern corporations shield the agents (board of directors) from oversight by the principals (shareholders). Consequently, directors tend to run the company for their own ends and shareholders get a raw deal.

Icahn likened the problem to a caretaker on an estate who refuses to allow the owner to sell the property because the caretaker might lose his job. The Icahn Manisfesto (as coined in his biography) proposed to shift the balance of power to benefit shareholders. If management turned a blind eye or deaf ear to his exhortations, he would push for control of the board.

His strategy was distilled into an investment memorandum that was distributed to prospective investors in 1976.

Icahn’s strategy is a combination of a hunt for value combined with shareholder activism. He tilts towards companies whose stock prices reflect a poor P/E ratio and whose book values exceed market valuation. Once he has narrowed down on a target, he begins to build upon his positions till he has a controlling stake. That done, he starts to push for changes which he believes would result in tremendous shareholder value. This would involve appointments on the board, management shakeups, rallying shareholder support, pushing for turnaround strategies, changes in CEO compensation, stock buybacks, divestiture of assets, and so on and so forth. He then benefits from obscene amounts of money when he finally exits.

Icahn pushed for the separation of eBay and PayPal in 2014. He believed that eBay was covering up the value of PayPal, and if it went public on its own, it would get a huge premium because of growth. eBay initially purchased PayPal in 2002 but Icahn felt that keeping them together was becoming less advantageous to each business strategically and competitively. The dynamic industry landscape resulted in each business facing different competitive opportunities and challenges. He got his way. In the third quarter of 2015, he swapped his equity stake in eBay for PayPal.

Is his strategy foolproof? Not at all. He lists Blockbuster as one of his more glaring mistakes.

Icahn's affair with Blockbuster actually started late 2004 when he began amassing a stake in the company and waged an attempt to get representation on the company's board. But he (and the board) underestimated the havoc the internet and online streaming would wreak on video stores. In 2007, he told Time magazine that Blockbuster's chain of stores was its greatest asset in the battle with Netflix.

Icahn finally gave up and his investment was flushed down the toilet. The Wall Street Journal reported with exact figures. He spent nearly $107 million to buy the company’s stock, and in 2010, offloaded almost his entire holding for a pitiful $3.4 million.

After he was done licking his wounds, he began to invest in Netflix and averaged at around $58 per share, in 2012. In 2015, he cashed out at around $677 levels.

In October 2013, Icahn declared that he owned 4.73 million Apple shares and reiterated his proposal that Apple should spend $150 billion to buy back its shares. In 2016, he dumped his Apple stock with a gain of some $2 billion in 32 months.

In both the above cases, he made a killing, but exited early. The shares continued to climb.

What can we learn from the above?

- You cannot win every single time. Every investor will have his share of bad investments.

- There is no way you can catch the top. If you find the stock is overvalued. And you have made a substantial gain. It is probably time to exit.

- You need to have skin in the game. Give your portfolio time. Study your investments. Track them.

- Have an investment philosophy. It will be your true north.

- Have an exit strategy. It will help you realise gains.