Sequence-of-returns risk, or sequence risk, is something that is grossly overlooked, but must never be ignored.

This is the risk that comes from the order in which your investment returns occur. Timing matters. If the stock market declines just before you retire and in the early years of your retirement, it truly hits your portfolio.

"Sequencing risk is the danger of a near-term decline in your assets causing you to over-withdraw, or the risk of a big decline early in your retirement wiping out a big part of your nest egg. This risk feels prominent in a recessionary environment," says Matt Wacher, CIO - Asia-Pacific, Morningstar Investment Management.

Just imagine: You have just retired. Inflation goes on. The stock market falls and so does the value of your equity portfolio. And now you have to start withdrawing from your savings to live. When you start making portfolio withdrawals, the value of your portfolio reflects both market performance and cash outflows. Not a great combination.

Different Sequence, Different Results

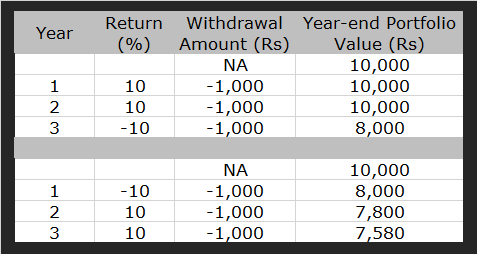

- Amount: Rs 10,000

- Amount you plan to withdraw: Rs 1,000 per year

If you earn 10% (first year), 10% (second year), and -10% (third year), you'd end up with Rs 8,000 by the end of the third year.

If you earn -10% (first year), 10% second year, and 10% (third year), you’d end up with Rs 7,580 by the end of the third year.

Under both scenarios the returns are identical, except that they are in reverse order. And the results are different. Why? Because the negative return at the beginning of the period (when more assets are in the account) carries more weight in the overall results. The portfolio doesn’t benefit as much in rupee terms from the two years of positive returns because there are fewer rupees remaining.

So what must retirees do?

Retirees have to draw a balance between sequencing risk and longevity risk. We don’t really know how long we need our capital to last for, so we need to maintain some level of growth assets.

The bucket approach that Morningstar's director of personal finance, Christine Benz, advocates is one way to mitigate the risk of an unfavorable sequence of returns. The central idea is to split your nest egg up into short-term, medium-term, and long-term buckets. By putting at least one or two years’ worth of planned withdrawals in a cash bucket, investors can guard against the risk of being forced to withdraw assets during a market downturn. This also leaves the remaining portfolio better positioned to rebound when the market eventually improves.

Matt advises on the longer-term bucket. "The longer-term bucket would carry more risk (equity), which will move higher and lower but will top-up your shorter-term buckets over time. The beauty of doing this is that is works really well with a valuation-driven asset allocation. This means favoring cheaper assets that are fundamentally attractive. These assets can often take a while to harvest but tend to have higher yields. If you get this approach right consistently, it has the potential to really add to your retirement cash flow over time."

Sequence-of-returns risk is one of the more underappreciated dangers of investing. Talk to your financial adviser to ensure that you are not overly exposed to the potential downside.

More by Investment Specialist and Senior Editor Larissa Fernand