We have constantly voiced the need to have a long-term perspective when investing in equity, as an asset class. To borrow from the old age, what really matters is time in the market rather than timing the market.

The reason being that over the long haul, the stock market's outperformance over cash boils down to just a few critical months. Miss those months and you will have missed all the risk premium to be earned from holding a volatile asset such as equities.

To see what actively managed funds look like from the critical months' perspective, we conducted a study that used active funds' returns over the 10-year period from October 2013 through September 2023.

Over this period, Indian stocks owed their outperformance over cash to just 12 months—10% of the months in the sample. If you held stocks for all 108 months apart from those 12 months, which we will call "critical months," you would not have beaten cash. On average, less than 4.2% of the months account for all of the outperformance for Indian actively managed diversified equity funds versus their benchmark.

(Our previous version of the study showed us that over another 10-year period (April 2012 to March 2022), Indian stocks owed all their outperformance over cash to just 11 months, or 9.2% of all months. Similar numbers were witnessed for actively managed funds, where, on average, just six months, or 5% of all months, accounted for their outperformance versus their benchmarks.)

Here is an excerpt from the report.

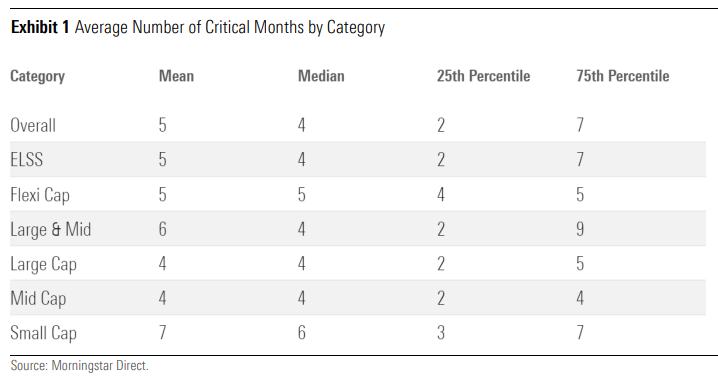

Exhibit 1 displays aggregate statistics for critical months, first in aggregate and then grouped by fund category. One can immediately see that whether it's mean, median, or the top- and bottom-quartile breakdowns, these numbers are small and should give little comfort to investors who try to find the best times to buy and sell actively managed funds. In aggregate, the median number of critical months was four. That means that half of the funds' outperformance was due to four or fewer months. One in four funds (25th percentile) owed their outperformance to only two months! Finally, three fourths (75th percentile) of all the funds' outperformance was attributable to seven or fewer months. Small-cap funds and large- and mid-cap funds were the best of the pack, while, expectedly, funds with a large-cap bias had the worst results.

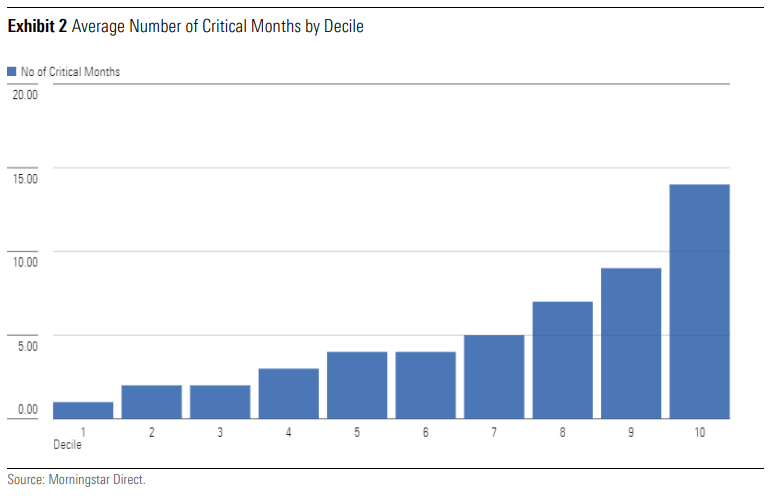

Finally, we divided funds by deciles of outperformance. Exhibit 2 shows how many critical months, on average, each decile had. Even the best decile of outperforming funds, on average, owed their outperformance to just 14 months of excess returns. That is one year and two months out of 10 years.

Disclaimer

© 2023 Morningstar. All rights reserved. The Morningstar name is a registered trademark of Morningstar, Inc. in India and other jurisdictions. This research on securities (“Investment Research”), is issued by Morningstar Investment Adviser India Private Limited. Morningstar Investment Adviser India Private Limited (CIN: U74120MH2013FTC249024), having its registered office at Platinum Technopark, 9th Floor, Plot No 17 & 18, Sector - 30A, Vashi, Navi Mumbai, Maharashtra, 400705, is registered with SEBI as a portfolio manager (registration number INP000006156), and research entity (registration number INH000008686).

Morningstar Investment Adviser India Private Limited has not been the subject of any disciplinary action by SEBI or any other legal/regulatory body. It is a wholly owned subsidiary of Morningstar Investment Management LLC, which is a part of the Morningstar Investment Management group of Morningstar, Inc. In India, Morningstar Investment Adviser India Private Limited has only one associate, viz., Morningstar India Private Limited, and this company predominantly carries on the business activities of providing data input, data transmission and other data related services, financial data analysis, software development etc.

The author/creator of this Investment Research (“Research Analyst”) or his/her associates or immediate family may have (i) a financial interest in the subject mutual fund scheme(s) or (ii) an actual/beneficial ownership of one per cent or more securities of the subject mutual fund scheme(s), at the end of the month immediately preceding the date of publication of this Investment

Research. The Research Analyst, his/her associates and immediate family do not have any other material conflict of interest at the time of publication of this Investment Research. The Research Analyst or his/her associates or his/her immediate family has/have not received any (i) compensation from the relevant asset manager(s)/subject mutual fund(s) in the past twelve months; (ii) compensation for products or services from the relevant asset manager(s)/subject mutual fund(s) in the past twelve months; and (iii) compensation or other material benefits from the relevant asset manager(s)/subject mutual fund(s) or any third party in connection with this Investment Research. Also, the Research Analyst has not served as an officer, director or employee of the relevant asset manager(s)/trustee company/ies, nor has the Research Analyst or associates been engaged in market making activity for the subject mutual fund(s).

The terms and conditions on which Morningstar Investment Adviser India Private Limited offers Investment Research to clients varies from client to client, and are spelt out in detail in the respective agreement. The Investment Research: (1) includes the proprietary information of Morningstar, Inc. and its affiliates, including, without limitation, Morningstar Investment Adviser India Private Limited; (2) may not be copied, redistributed or used, by any means, in whole or in part, without the prior, written consent of Morningstar Investment Adviser India Private Limited; (3) is not warranted to be complete, accurate or timely; and (4) may be drawn from data published on various dates and procured from various sources. No part of this information shall be construed as an offer to buy or sell any security or other investment vehicle. Neither Morningstar, Inc. nor any of its affiliates (including, without limitation, Morningstar Investment Adviser India Private Limited), nor any of their officers, directors, employees, associates or agents shall be responsible or liable for any trading decisions, damages or other losses resulting directly or indirectly from the use of the Investment Research. Investments in securities market are subject to market risks. Read all the related documents carefully before investing. Wherever any securities are quoted, they are quoted for illustration only and are not recommendatory.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The Morningstar Medalist Rating is the summary expression of Morningstar’s forward-looking analysis of investment strategies as offered via specific vehicles using a rating scale of Gold, Silver, Bronze, Neutral, and Negative. The Medalist Ratings indicate which investments Morningstar believes are likely to outperform a relevant index or peer group average on a risk-adjusted basis over time. Investment products are evaluated on three key pillars (People, Parent, and Process) which, when coupled with a fee assessment, forms the basis for Morningstar’s conviction in those products’ investment merits and determines the Medalist Rating they’re assigned. Pillar ratings take the form of Low, Below Average, Average, Above Average, and High. Pillars may be evaluated via an analyst’s qualitative assessment (either directly to a vehicle the analyst covers or indirectly when the pillar ratings of a covered vehicle are mapped to a related uncovered vehicle) or using algorithmic techniques. Vehicles are sorted by their expected performance into rating groups defined by their Morningstar Category and their active or passive status. When analysts directly cover a vehicle, they assign the three pillar ratings based on their qualitative assessment, subject to the oversight of the Analyst Rating Committee, and monitor and re-evaluate them at least every 14 months. When the vehicles are covered either indirectly by analysts or by algorithm, the ratings are assigned monthly. For more detailed information about the Medalist Ratings, including their methodology, please go to the section titled “Methodology Documents and Disclosures” at http://global.morningstar.com/managerdisclosures.